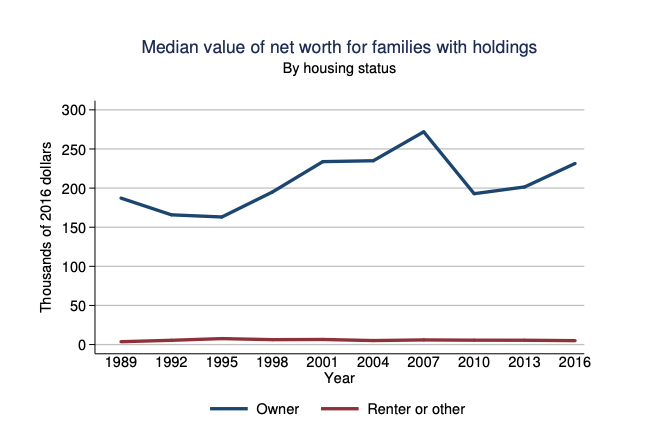

In the Federal Reserve’s most recent Survey of Consumer Finances (in 2016), a blockbuster statistic was revealed. The median net worth of homeowners was $231,400. Renters had a net worth of just $5,000.

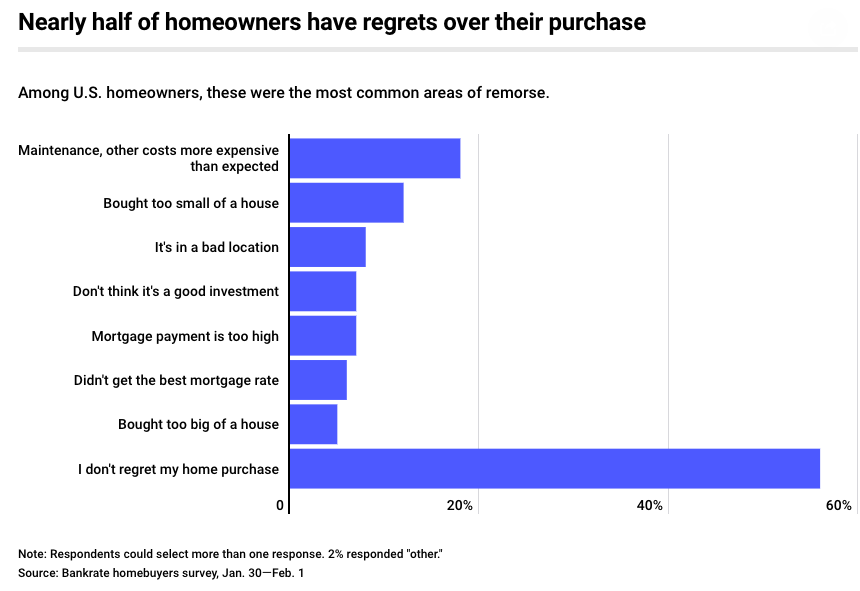

This powerful statistic would suggest that everyone should run out and purchase a home now. However, in a study by Bankrate, it was discovered that 2/3rds of Millennials (63%) regretted purchasing a home, with almost half of all homeowners (44%) expressing the same sentiment. If homeownership is so strongly associated with wealth, then why aren’t more people happy about it?

During the Great Recession, millions of homeowners lost far more than their investment, when they saw their home values plunge to a fraction of what they had paid. Millions of homes were auctioned off, foreclosed upon or went through a short sale process. Today, even with real estate prices higher than ever, 5 million properties (8.8% of U.S. homes with a mortgage) are still severely underwater, i.e. with mortgages on the hook for 25% or more than the value of the property.

So, successful home ownership is not just a matter of getting in the game. It requires a smart strategy. Everyone who purchased in 2006 saw the value of her property decline severely and rapidly. Almost everyone who purchased in 2009 is living in the lap of equity luxury today.

8 Things To Know Before You Buy or Sell in 2019.

Real Estate Prices are Higher Than Ever.

Real Estate is Local.

Unaffordability and Sales Statistics.

Millennials Delaying Purchase.

The Mortgage Interest Rate Deduction

Tips for Successful Home Ownership

The High Price of Free Advice

Climate Change

And here’s more information on each point.

8 Things To Know Before You Buy or Sell in 2019.

Real Estate Prices are Higher Than Ever.

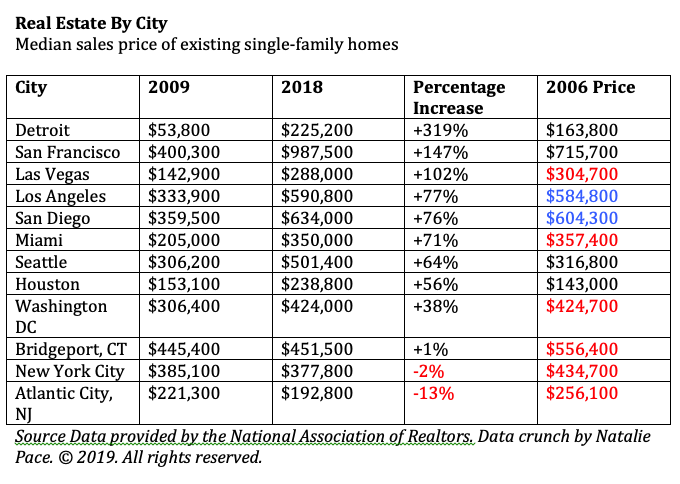

Since 2009, home prices are up 47% nationwide. At $253,600, the median sales price of existing homes is 14% higher than the top of the market in 2006 (source: The National Association of Realtors). In many cities, prices have become unaffordable to the locals. It’s never a good idea to buy high.

Real Estate is Local.

Cities like San Francisco, Las Vegas and Detroit have seen real estate values double off of the lows. The Eastern seaboard has seen tepid increases and even declines in some areas. Ground zero cities for the Great Recession real estate implosion, such as Las Vegas and Miami, are still underwater. Along the West Coast, and in other hot areas like Denver, real estate has posted outstanding gains over the last decade, but has become unaffordable to the locals.

Unaffordability and Sales Statistics.

In 2018, home sales were 3% lower than they were in 2017, although prices are still rising. It’s too early to tell if this is the beginning of a decline, or just a leveling off. However, as Lawrence Yun, the chief economist of the National Association of Realtors, told me in an interview last month, “The unaffordability is making home sales plunge in California, even though the job market is great. Unless California can address the unaffordability of housing, you may see people leaving the area.” Yun recommends that everyone, particularly recent college graduates, consider quality of life and the cost of living when deciding which job to accept. According to Yun, “A salary of $100,000 in San Francisco will not go a long way. A lower salary of $80,000 in Atlanta or Nashville will go a much further distance because housing costs are much lower.”

Millennials Delaying Purchase.

In a recent survey, the National Association of Realtors discovered that Millennials are delaying their first home purchase by five years. First time home buyers typically make up 40% of the buying pool. However, in 2018 that percentage was just 30%. Two of the main reasons that Millennials are delaying home purchase are the high cost of paying off their student loans and that home prices are unaffordable for them. What many Millennials may not know is that buying a home can dramatically reduce the amount they pay in taxes.

The Mortgage Interest Rate Deduction

Homeowners in the U.S. qualify for a mortgage interest rate deduction on their taxes, for home values up to $750,000. Recent tax laws have reduced the property tax deduction, which has played into why home values are tepid or down along the Eastern seaboard. However, in general, the sooner you can start claiming this tax write-off, the quicker you will stop making the taxman rich, and start building up your own wealth and home equity.

Tips for Successful Home Ownership

Here are a few general rules

for successful home ownership.

1. Buy what you can afford.

2. Make sure that you understand the dynamics of the local marketplace.

3. Pick a leader. Every city has that one address where all of the bad luck seems to congregate.

4. Do the math yourself. You don’t want hidden costs and problems to show up after you are on the deed.

5. Get a fixed rate. Don’t stretch to get into a home with an adjustable-rate mortgage.

6. Buy low. Beware of buying at the top of a business cycle!

7. Align your pay-off date with your retirement date. If you are retiring in 10-years, you don’t want a 30-year mortgage. Once you go on fixed income, you want your costs to be reduced, so that you can easily afford your life as a retiree.

The High Price of Free Advice

Do the math and read the fine print. Behind every purchase are insurance costs, maintenance repairs, property taxes, plumbing/roof fixes and other expenses that don’t show up on the beautiful brochure. Realtors are incentivized to sell you something (for their commission). Real Estate educators want to sell you into their seminars – without regard as to whether or not you’ll make a successful purchase. Trump University wasn’t the only seminar program selling expensive educational products and encouraging investors to buy and flip before the real estate bubble popped.

Climate Change

Climate change is affecting real estate all across the U.S. Along the coasts, homeowners are impacted by rising seas and erosion. Droughts are longer and more severe in the arid regions. Some areas have unsustainable water plans and are already fighting over the rights to certain rivers. Some regions, like Sarasota, Florida, are being required to disclose climate change issues. It’s a good idea to sound what opportunities and challenges might be realized over the next decade in the neighborhood you are interested in purchasing.

So is Real Estate the Fast Track to the Rich House or the Poor House?

There is no doubt that real estate is a rocket-propelled ride to wealth, but only when you purchase for a good price, buy what you can afford and don’t get sucked into a money pit of maintenance costs. Getting all of those factors right will require more information, research and reflection than most salesmen will offer you. Once you’ve signed on the dotted line and paid up, all of the blessings and challenges are yours alone. Financial lives can be ruined (and lost), and commissions will still be paid to the mortgage broker and realtor. So, you have to be the boss of your money and the boss of the process to be sure that you are buying what is right for you, at this moment in your career path.

Learning the opportunities and challenges from the experts can be invaluable to the process. Go to BlogTalkRadio.com/NataliePace to access my full interview with Lawrence Yun.

If you are interested in learning more about successful home purchase, join me at my Real Estate Master Class April 26, 2019 in Denver, Colorado. Call 310-430-2397 or email [email protected] to learn more.