The internet has changed the way we communicate with each other and allowed us to connect to each other globally, democratised information and now this technology is helping to solve some of the world’s greatest problems through cryptocurrencies; which has the potential to change the lives of some of the world’s poorest and most desperate communities for the better.

Hyperinflation, poverty, lack of jobs, lack of access to banking, lack of capital and poor access to markets are among the problems that cryptocurrencies can to solve. It can improve lives by helping people within developing countries participate in the global economy and escape from poverty. This will be achieved by giving everybody worldwide the access to modern banking and financial services through blockchain, a counterpart to cryptocurrencies.

There are many entrepreneurs, economists, aid officials and bankers who believe a combination cryptocurrency and mobile phones, will give the world’s poor access to the global economy and overcome many of the traditional banking’s limitations.

For example, local farmers in small villages in rural Africa, don’t have access to a personal form of ID, nor a bank account and for them it seems that at every step there is something that makes their lives a little bit more difficult. Yet, this is the reality for millions of people all across Africa and many other emerging countries. The “smartphone coverage” within these regions however is progressing at an extremely fast pace. These people have no or limited access to saving products, insurance, international markets and convenient payment methods. This means they have little understanding of how to participate in the global economy, which will eventually allow them to escape from poverty. Shockingly, data from the World Bank shows that 1.7 billion people do not have a bank account; that is 31% of the adult world population.

This is why financial inclusion is critical factor of economic growth and plays a major role in eroding poverty. It enables to reduce the gap between rich and poor populations; can boost job creation, accelerate consumption. It can directly help vulnerable people manage risk and absorb financial shocks. This why the United Nations (UN) is exploring the idea of using blockchain technology to provide legal entities to over one billion people without any authorised documents. For example, this year, its World Food Program is using cryptocurrency for payments to 500,000 refugees. As many of today’s refugees have mobile phones but no access to banks.

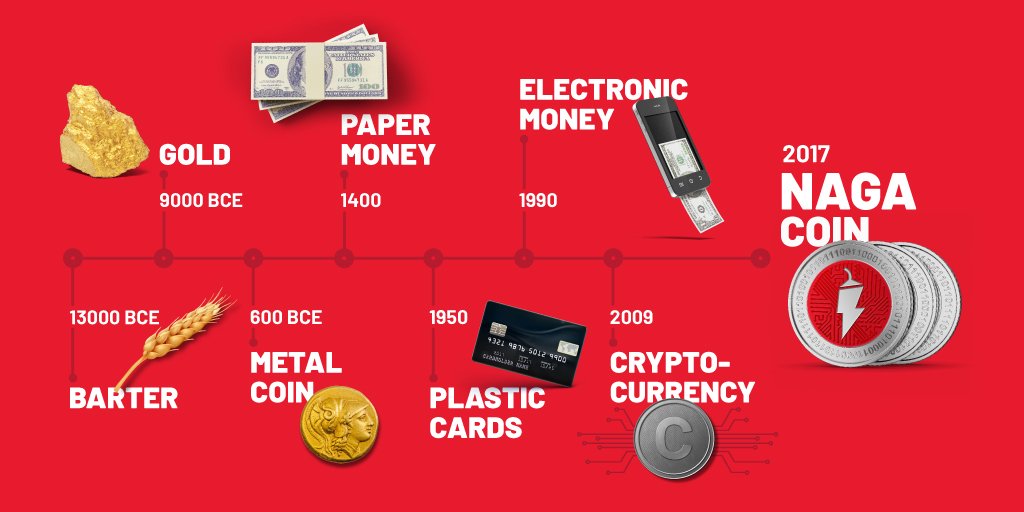

Fintech companies like The NAGA Group AG have developed mobile finance solutions that will bring cryptocurrencies to the mainstream masses, including the unbanked populations across the globe. At NAGA, our publicly listed company has put financial inclusion – across asset classes and continents – at the heart of its mission and works on innovations that will enable users to send and receive cryptocurrency payments via email or phone numbers and convert these into cash. We believe that no resource is truly scarce and that instead a world of abundance, is nothing more than a matter of accessibility.

Unlike banks, no physical branch presence is needed for blockchain to work. Since the technology operates on a distributed network, there’s no need for a complex, opaque and expensive private infrastructure to run. This saves on the costs that banks pass on to users through fees and other charges when using bank accounts or performing mobile transactions.

With mobile financial technology, suddenly financial services are available to anyone with a mobile phone at a fraction of the cost.

We have also developed The NAGA WALLET – a revolutionary cryptocurrency wallet that will give clients a fast and affordable way to access and manage crypto assets thanks to features such as instant, real-time transactions and up to 50% lower transaction fees when using the NAGA COIN – our own in-house-token. Plus, while most other wallets only support a few currencies, The NAGA WALLET supports five coins and more than 1,200 tokens.

Financial technology is even more important in our current globalized world, where migration of people from one country to another for employment has become common practice. For example, in India with almost 16 million people, it has the largest diaspora in the world. These workers are an economic boon for India’s economy, because they send money to their relatives and friends at home. In 2017, India remained the world’s top transfer recipient country, amounting to $69 billion. However, the problem, is that the global remittance industry and money transfer operators charge high fees on money sent abroad, which is cutting off a lifeline for the vulnerable people tackling socio-economic problems. Yet it is cryptocurrency that can provide the solution, as it can improve the customer’s remittance experience by increasing the speed and crucially by reducing the transaction costs! It has the potential to offer peer-to-peer payment transactions for a low, flat fee to people who put money in the hands of their loved ones.

It is very clear that cryptocurrency can bring a large percentage of the world’s poor into the 21st Century, allowing them to participate in the global economy, giving them the opportunity to save money, earn interest, invest, start a business, borrow money, receive remittances, or send money to friends and family for the first time. The effect of this will be enormous and it can lead to millions of new businesses and vast amounts of new wealth, which is a good thing for us all.