Golden Years Are Looking Considerably Less Golden

Fact #1: We are saving less as a society. Here is a chart from the St. Louis Fed showing the steep decline in personal savings rates over the last few decades.

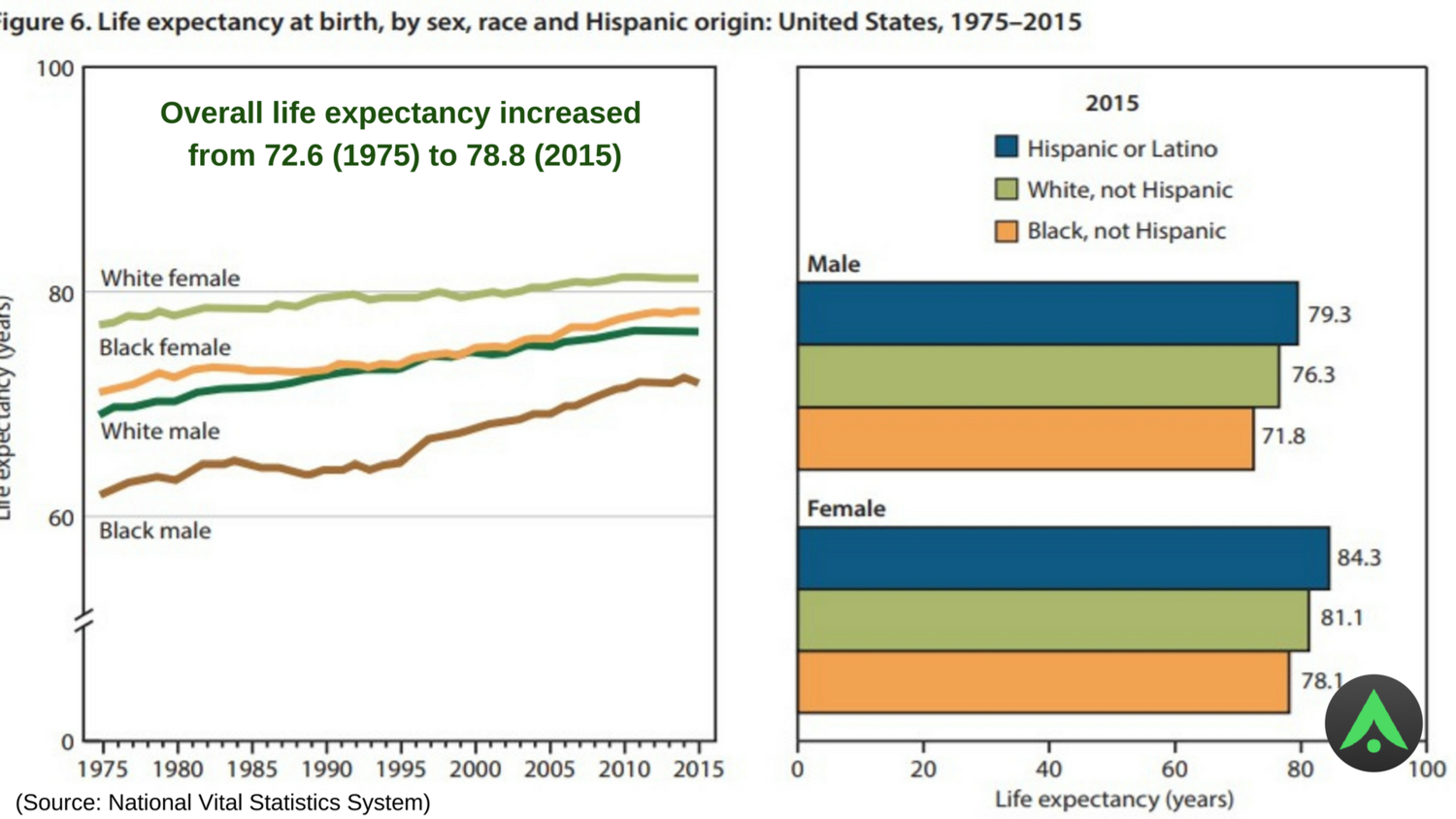

Fact #2: We are living longer. Life expectancy in the US has risen almost 7% over the last 40 years as the chart below shows. This is good news actually – but it puts additional pressure on the need to save (and, on social safety nets).

Fact #3: Automation and Robots Will Replace Human Workers. Robots and automation will displace large swaths of American workers (e.g., truck drivers getting replaced by driver-less trucks, etc.).

The robot/automation revolution will take a long time to play out – about 40 years or so. See here and here as example articles to show the breadth and scope of industries where automation is making inroads.

Taken together, this means that for most seniors, golden years will cease to be “golden.” Those with inadequate savings may be required to get back into the work-force, or seek assistance from their family — alternatives that many may find distasteful.

Answer: Save More. Early.

The answer clearly is to save more early. But most people don’t do this — waiting until it’s too late. Reasons for delaying range from:

- Lack of awareness of the importance of saving.

- Under-estimating the compounding effect of small savings today over long periods.

- Believing incorrectly that social security and other social safety net will be adequate to cover retirement needs.

- Believing incorrectly that current financial situation does not allow any savings (“I am living pay check to pay check. Nothing left over to save.”).

- Believing incorrectly that good times in youth will continue. In fact, as one gets older, life becomes considerably more difficult — health issues crop up, financial commitments increase (kids’ education, elder care for parents, etc.), skills potentially atrophy and jobs become harder to come by.

6-Step Plan to Building a Savings Habit

At Arnexa, we have come up with a 6-step plan to helping people build a savings habit. It’s obvious but provides a good framework to work within to help users.

Step 1: Identify “savings” purpose

The first step is in fact both the hardest and most important. Stephen Covey in his landmark 7 Habits of Highly Effective People calls this step “Begin with the end in mind.”

A journey of a thousand miles begins with a single step. (Laozi)

Purpose tells you clearly what you are going to achieve, why and the impact of failure. It keeps you on track when the going gets tough (as it surely will).

Your “Purpose” in saving could be many. Examples include — “retirement,” “kids college fund,” “rainy day fund,” etc.

Be also very clear about what happens if your purpose is thwarted — in other words, if you fail. Paint this picture in stark terms and don’t sugar coat it. Examples:

“If I don’t have enough for my retirement, I will be screwed: I will have to rely on my children for retirement. Or go back to work at a time in my life when I may be most ill-prepared to do so.”

“If I don’t save enough for my a rainy day, I will be forced to pay exorbitant interest rates to get short-term loans to cover emergency expenses. Which will put me further into the hole.”

“If I don’t save enough for my kids education, I will feel like a dead-beat parent. I will be giving them a worse future than my parents gave me.”

Step 2: Build “commitment” to save for the stated purpose.

Think of commitment as a reservoir of your resolve to achieve your stated purpose. Commitment can rise and fall over time esp. as goals become harder to achieve. Think of a classic example from weight-loss. Your purpose may be “I will become healthier by losing weight.” Your commitment is most full on New Year’s Day as you buy all the expensive gizmos to help you. The daily grind then wears you down as you skip exercise more and more regularly. Interestingly, your commitment can rise if someone comments on how good you look.

When your commitment (or, reservoir) is empty, you can no longer fulfill your purpose!

The stronger your savings purpose, the more full your commitment reservoir starts out. Then, as you meet goals, achieve small successes and accumulate accolades, these fill up your commitment reservoir. This is why it is also super important that your initial steps lead to success. Early failure is disheartening — and can deplete the commitment reservoir pretty quickly.

Steps 3 & 4: Set “bite-sized” goals and milestones.

Set your initial goals to be easy, perhaps even laughably so. With respect to your savings goals, even small amounts compound so you are completely OK in setting initial small, non-ambitious, easy goals. Over time, you can ratchet up the goal difficulty. Set the goals to be for small amounts over small time periods. Instead of a goal “I will save $30 this month” you could say “I will save $7.50 this week,” or even better “I will save $1 a day.” Goals and activities you undertake need to be burned into your “muscle memory.”

Organizing yourself to meet your goal so that you have clear milestones to achieve it are crucial. Put these milestones down on your mobile app calendar so that calendar reminders will serve as a reminder in case you are about to miss a milestone. Resolve not to miss milestones — for missing a milestone will make the next milestone doubly hard!

Step 5: Celebrate goal success.

Achieving your goals (no matter how small or simple or easy) is worthy of celebration. When someone gives you a “High 5” for meeting your goal, you feel good. This “feel good” vibe replenishes your commitment reservoir.

So you should celebrate when you meet your own goals. Give yourself a treat (an inexpensive one, please :-)).

But it is also vital that you celebrate other people meeting their goals. When you congratulate others who meet their goals, they feel good and will be more likely to meet their own goals. But remember, that they in turn will likely congratulate you on your successes thereby reinforcing your commitment.

Reciprocity (as in other walks of life) works here as well. Be generous in your praise of others even if they save smaller amounts than you. Their financial situation may be more precarious than yours so that their achievement in saving small amounts is actually considerable!

Step 6: Compete and win!

When you start doing well on your goals and get into a “groove,” slowly ratchet up the savings difficulty so that you are saving more over shorter time periods. In the Arnexa app, you can see where you stack up compared to others on the leader board.

If you do not have the Arnexa app and/or don’t want to use it, join a group of other committed savers so that each of you can reinforce the other. When others like you are better savers, it will inspire you to do better as well. Like a gym partner who forces you to do that extra rep!

The Arnexa app codifies this 6-step process in a free iPhone app (no ads, no spam) that we believe is easy to use and may help you build the savings habit. Try it now.

Summary & Conclusion

Sweeping changes in society make saving money ever more important. It’s good news that some of these changes will take a long time to take effect. We need to use this time to build up our savings. Like Noah, we need to start building our proverbial Ark now. #PrepareNow.