Many Americans are feeling increasingly uneasy about their ability to keep up with debt payments. According to new research from the New York Fed, expectations of missed minimum payments are close to their highest levels in over a decade, excluding pandemic-related spikes. Studies from the Fed, CFPB, and academic experts show that rising financial stress and uncertainty can increase the risk of missed payments—while tools that promote visibility and planning can ease stress and improve outcomes. Helping people reduce financial stress is central to SuperMoney’s mission.

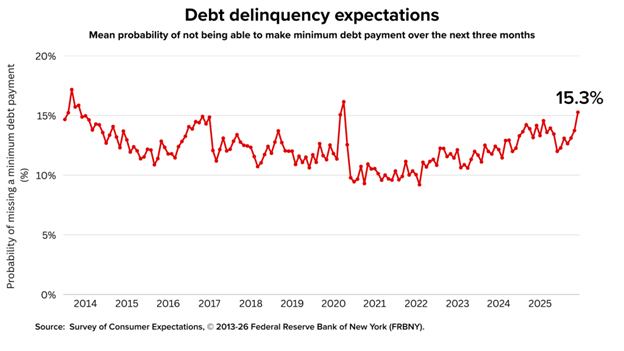

As debt anxiety grows across the country, SuperMoney is doubling down on our mission to help Americans regain control of their finances. The latest Survey of Consumer Expectations from the New York Federal Reserve shows that households now see a greater risk of missing a minimum debt payment than at nearly any time in the past 10 years, outside of the pandemic.

These figures don’t reflect delinquencies themselves—they’re a signal of something just as important: mounting stress and financial uncertainty.

Debt payment worries reach a critical threshold

In December 2025, Americans reported an average 15.3% chance of missing a minimum debt payment within the next 90 days. That’s one of the highest readings since the Fed began tracking the data more than a decade ago, excluding the upheaval of the COVID-19 crisis.

Historically, shifts like this foreshadow actual delinquencies. As household budgets tighten and financial flexibility disappears, people tend to feel pressure well before missed payments show up on credit reports.

These stress signals are often the canary in the coal mine.

Why so many households feel squeezed

Other data helps explain why delinquency fears are rising. PNC Bank reports that 67% of U.S. workers live paycheck to paycheck. That leaves little cushion for surprise expenses or rate hikes. Meanwhile, credit metrics show that subprime lending has bounced back to pre-pandemic levels—and more than a quarter of Americans now have non-prime credit.

In short, the post-pandemic “recovery” hasn’t done much to ease financial strain for millions of families. While credit access has normalized, personal finances are still stretched thin.

How stress and uncertainty affect payment habits

Behavioral economics offers a powerful explanation: when financial uncertainty is high, people tend to avoid making decisions—even when their income and debt remain stable. According to research from the National Bureau of Economic Research, this uncertainty makes it harder to stay on top of bills or confront rising balances.

The Consumer Financial Protection Bureau backs this up. Their findings show that consumers with low financial well-being are far more likely to fall behind on payments and struggle to manage day-to-day finances. Put simply, when people feel financially overwhelmed, it becomes harder to act.

That’s why reducing stress and promoting financial clarity is a core focus at SuperMoney.

Small changes can make a big difference

A landmark field experiment by the Federal Reserve Bank of Boston found that basic reminders and improved attention to debt helped struggling consumers lower balances and boost their credit scores—by an average of 20 points—without changing their income or education.

Additional Fed research shows that people who regularly check their account balances and stay aware of upcoming bills tend to avoid fees and carry less revolving debt. Across the board, the data support one message: visibility leads to better financial outcomes.

That’s why budgeting is so effective. When you understand where your money is going, you can make adjustments early—before a missed payment turns into long-term damage.

The current outlook: anxiety rising before delinquencies

The New York Fed’s data shows a rising tide of concern, even before missed payments spike in credit data. As families face growing costs and tighter budgets, the ability to plan and stay organized becomes even more essential.

SuperMoney’s goal is to help people reduce uncertainty before it turns into ca risis. Tools that make finances more transparent—like spending trackers and budgeting apps—can help prevent small setbacks from becoming credit disasters.

How SuperMoney supports financial peace of mind

With more than 25% of Americans holding non-prime credit and the majority living paycheck to paycheck, financial stability often hinges on awareness and consistency. Knowing what’s due, what’s left, and what’s coming next can make all the difference.

That’s why SuperMoney developed a free financial app that helps users stay ahead of bills, track spending, and reduce the stress that uncertainty creates. Our mission is simple: empower people with the tools they need to stay financially healthy and focused.

Explore the SuperMoney app and take the first step toward greater financial clarity.

Key takeaways:

- Delinquency expectations are near decade highs, reflecting growing financial stress.

- Consumers reported a 15.3% chance of missing a minimum payment in December 2025.

- Behavioral research shows that stress and uncertainty raise delinquency risks.

- Simple tools—like reminders and budgeting—can significantly improve payment behavior.

Sources:

- Survey of Consumer Expectations – Federal Reserve Bank of New York

- Financial well-being research – Consumer Financial Protection Bureau

- Nudging credit scores in the field – Federal Reserve Bank of Boston

- Behavioral economics and consumer finance papers – National Bureau of Economic Research